Future and forward contract as a route of hedging the risk

Abstract

In the present highly uncertain business scenario, the importance of risk management is much greater than ever before. Variations in the prices of agricultural and non-agricultural commodities are induced, over time, by demand-supply dy namics. The last two decades have witnessed many-fold increase in the volume of international trade and business due to the wave of globalization and liberalization sweeping across the world. This has led to rapid and unpredictable variations in financial assets prices, interest rates and exchange rates, and subsequently , to exposing the corporate world to an unwieldy financial risk. As a result, financial markets have experienced rapid variations in interest and exchange rates, stock market prices thus exposing the corporate world to a state of growing financial risk. The emergence of derivatives market is an ingenious feat of financial engineering that provides an effective and less costly solution to the problem of risk that is embedded in the price unpredictability of the underly ing asset. Derivatives provide an effective solution to the problem of risk caused by uncertainty and volatility in underly ing assets. These are the financial instruments that are linked to a specific financial instrument or indicator or commodity and through which specific risks can be traded in financial markets in their own right. In actual practice there are various different types of derivatives but this paper emphasizes on the two most important ty pes of derivatives i.e. futures and forward contracts. These two are the most commonly used types of derivatives in financial markets. We can hedge the risk of price variations in stocks, bonds, commodities, currencies, interest rates, market indices etc. This study is about the futures and forward contracts. This paper presents various ty pes of futures and forward contract and what advantages and disadvantages these two important types of derivatives have? It also includes that how futures and forward contacts can be used as hedging tools of risk management.

Key words: Underlying assets: The underlying asset is the financial instrument (e.g., stock, futures,

commodity, currency, index etc.) on which a derivative's price is based. Hedge: Hedge means making an investment to reduce the risk of adverse price movements in an asset. Long position: The party who agrees to buy in the future is said to hold long position. Short position: The party who agrees to sell in the future is said to hold a short position. Payoff: The gain attained or the loss incurred by the holder of a future orforward contract at delivery date.

Introduction

In the present highly uncertain business scenario, the importance of risk management is much greater than

ever before. The last two decades have witnessed many-fold increase in the volume of international trade and business due to the wave of globalization and liberalization sweeping across the world. This has led to rapid and unpredictable variations in financial assets prices, interest rates and exchange rates, and

subsequently, to exposing the corporate world to an unwieldy financial risk. Increased financial risk causes losses to an otherwise profitable organization. This underlines the importance of risk management to hedge against uncertainty. Derivatives are risk management tools that help an organization to effectively transfer risk. The derivatives provide an effective tool to the problem of risk and uncertainty due to fluctuations in interest rates, exchange rates, stock market prices and the other underlying assets.The derivative markets have become an integral part of modern financial system.

Methodology of Research

This study is based on secondary data and empirical research of authors. Being teachers of derivatives

whatever we come across in teaching to the students we have tried to inculcate the problems and trade

mechanis m in derivative trading. Several valuable sources consist of books, websites and research papers

have been taken into account to enlighten the learners of derivatives. This paper will definitely be helpful for the beginners and teachers as well

Concept of Derivatives

The derivatives originate in mathematics and refer to a variable which has been derived from another

variable. So a derivative is a security whose price is dependent upon or derived from one or more

underlying assets. The derivative itself is merely a contract between two or more parties. Its value is

determined by fluctuations in the underlying asset. The most common underlying assets include stocks,

bonds, commodities, currencies, interest rates and market indexes. Most derivatives are characterized by

high leverage. Futures contracts, forward contracts, options and swaps are the most common types of

derivatives. Derivatives are contracts and can be used as an underlying asset. There are even derivatives

based on weather data, such as the amount of rain or the number of sunny days in a particular region.

Section 2(ac) of Securities Contract Regulation Act (SCRA) 1956 defines Derivative as:

a) A security derived from a debt instrument, share, loan whether secured or unsecured, risk instrument or contract for differences or any other form of security;

b) A contract which derives its value from the prices, or index of prices, of underlying securities.

The International Monetary Fund (2001) defines derivatives as “financial instruments that are linked to a specific financial instrument or indicator or commodity and through which specific risks can be traded in financial markets in their own right. The value of a financial derivative derives from the price of an underlying item, such as an asset or index. Unlike debt securities, no principal is advanced to be repaid and no investment income accrues.”

Underlying Asset in a Derivatives Contract

As defined above, the value of a derivative instrument depends upon the underlying asset. The underlying asset may assume many forms:

1.Commodities including grain, coffee beans, orange juice;

2.Precious metals like gold and silver;

3.Foreign exchange rates or currencies;

4.Bonds of different types, including medium to long term negotiable debt securities issued by governments, companies, etc.

5.Shares and share warrants of companies traded on recognized stock exchanges and Stock Index.

Benefits of Derivatives

1.They help in transferring risks from risk adverse people to risk oriented people.

2.They help in the discovery of future as well as current prices.

3.They catalyze entrepreneurial activity.

4.They increase the volume traded in markets because of participation of risk adverse people in greater numbers.

5.They increase savings and investment in the long run.

Participants in Derivatives Market

1.Hedger:A hedger is a trader who enters the derivative market to reduce a pre- existing risk. In India, most derivatives users describe themselves as hedgers and Indian laws generally require the use of

derivatives for hedging purposes only.

2.Speculators: A speculators, the next participant in the derivative market, buy and sell derivatives to bookthe profit and not to reduce their risk. They wish to take a position in the market by betting on future price volatility of an asset. Speculators are attracted to exchange traded derivative products because of their high liquidity, high leverage, low impact cost, low transaction cost and default risk

behavior. Futures and options both add to the potential gain and losses of the speculative venture. It is the speculators who keep the market going because they bear the risks, which no one else is willing to bear.

3.Arbitrageur: The third participant, arbitrageur is basically risk-averse and enters into the contracts,

having the potential to earn riskless profits. It is possible for an arbitrageur to have riskless profits by buying in one market and simultaneously selling in another, when markets are imperfect (long in one

market and short in another market). Arbitrageurs always look out for such price differences. Arbitrageurs fetch enormous liquidity to the products which are exchange traded. The liquidity in -turn

results in better price discovery, lesser market manipulation and lesser cost of transaction. Hedgers,speculators and arbitrageurs all three must co-exist. In simple words, all the three type of participants are required not only for the healthy functioning of the derivative market, but also to increase the liquidity in the market. The market would become mere tools of gambling without the hedgers, as they provide economic substance to the market. Speculators provide depth and liquidity to the market. Arbitrageurs help price discovery and bring uniformity in prices.

Applications of Financial Derivatives

Derivatives market plays a significant role in managing the financial risk of the corporate business

world. Financial derivatives have been very useful, popular and successful innovations in capital markets

all over the world. Recently, it is noted that financial derivative markets have been actively functioning in both developed as well as developing countries.

Following are the important functions:-

Hedging

The primary application is hedging which is also known as price insurance, risk shifting or risk transference function. They provide a vehicle through which the traders can hedge their risks or protect

themselves from the adverse price movements in the underlying assets in which they deal. For example, a

farmer bears the risk at the market to hedge the risk by selling a futures contract. For instance, if he is expected to produce 1000 tons of wheat in next six months, he could establish a price for that quantity by selling 10 wheat futures contracts, each being of 100 tons. In this way by selling these futures contracts, the farmer intends to establish a price today that will be harvested in the futures.

Price discovery

It means revealing of information about futures cash market prices through the futures market. As we know that in this market, a trader agrees to receive or deliver a given commodity or asset at a certain futures

time for a price which is determined now. It means that the futures market creates a relationship between

the future price and the price that people expect to prevail at the delivery date.

The traders can compare the spot and futures prices and will be able to decide the optimum allocation of their quantity of underlying asset between the immediate sale and futures sale.

This function is very much useful for producers, farmers, cattle ranchers, etc.

Financing

This means to raise finance against the stock of assets or commodities. Since futures contracts are

standardized contracts, so they make it easier for the lenders about the assurance of quality, quantity and liquidity of the underlying asset. This function is very much familiar in the spot market, but it is also unique to futures markets.

Liquidity

As we see that the main function of the derivative market deals with such transactions which are matured in the future period. They are operated on the basis of margins which are determined on the basis of rides involved in the contract. Under this the buyer and the seller have to deposit only a fraction of the

contract value, say 5 percent or 10 percent, known as margins. It means that the traders in the derivative

market can do the business a much larger volume of contracts than in a spot market and thus, makes market

more liquid. That is why; the volume of the futures markets is much larger in comparison to the spot

markets. This is also known as gearing or leverage factor.

Price stabilization

Another important function is to keep a stabilizing influence on spot prices by reducing the amplitude of short term fluctuations. In other words, derivatives market reduces both the heights of the peaks and the depth of the troughs. The major causative factors responsible for such price stabilizing influence are such as speculation, price discovery, etc.

Disseminating information

Derivative markets disseminate information quickly, effectively and inexpensively and as a result, reducing the monopolistic tendency in the market. Further such information disseminating service enables the society to discover or form suitable true/ correct/ equilibrium prices. They serve as barometers of futures in price resulting in the determination of correct prices on spot markets now and in futures.

Classification of Derivatives Market

Derivative markets can broadly be classified as

1.Commodity Derivative Market

2.Financial Derivative Market

As the name suggest, commodity derivatives markets trade contracts for which the underlying asset is a commodity. It can be an agricultural commodity like wheat, soybeans, rapeseed, cotton, etc. or precious

metals like gold, silver, etc.

Financial derivatives markets trade contracts that have a financial asset or variable as the underlying.

The more popular financial derivatives are those which have equity, interest rates and exchange rates as

the underlying. The most commonly used derivatives contracts are forwards and futures which we shall

discuss in detail later.

Forward Contracts

A forward contract is an agreement between two parties – a buyer and a seller to purchase or sell something at a later date at a price agreed upon today. Forward contracts, sometimes called forward

commitments, are very common in everyone life. Any type of contractual agreement that calls for the future

purchase of a good or service at a price agreed upon today and without the right of cancellation is a

forward contract. Forward is just a contract to deliver at a future date (exercise date or maturity date) at a specified exercise price.In forwards, no money changes at the time of deal. At the time the forward

contract is written, a specified price is fixed at which asset is purchased or sold. This specified time is referred as delivery price.

Features of forward contract

The basic features of a forward contract are given in brief here as under:

Bilateral: Forward contracts are bilateral contracts, and hence, they are exposed to counterparty

risk.

More risky than futures: There is risk of nonperformance of obligation by either of the parties, so these are riskier than futures contracts.

Customized contracts: Each contract is custom designed, and hence, is unique in terms of contract size, expiration date, the asset type, quality, etc.

Long and short positions: In forward contract, one of the parties takes a long position by agreeing to buy the asset at a certain specified future date. The other party assumes a short position by agreeing to sell the same asset at the same date for the same specified price. A party with no obligation offsetting the forward contract is said to have an open position. A party with a closed position is, sometimes, called a hedger.

Delivery price: The specified price in a forward contract is referred to as the delivery price. The forward price for a particular forward contract at a particular time is the delivery price that would apply if the contract were entered into at that time. It is important to differentiate between the forward price and the delivery price. Both are equal at the time the contract is entered into. However, as time passes, the forward price is likely to change whereas the delivery price remains the same.

Synthetic assets: In the forward contract, derivative assets can often be contracted from the combination of underlying assets, such assets are often known as synthetic assets in the forward market. The forward contract has to be settled by delivery of the asset on expiration date. In case the party wishes to reverse the contract, it has to compulsorily go to the same counter party, which may dominate and command the price it wants as being in a monopoly situation.

Pricing of arbitrage based forward prices: In the forward contract, covered parity or cost-of-carry relations are relation between the prices of forward and underlying assets. Such relations further assist in determining the arbitrage-based forward asset prices.

Popular in FOREX market: Forward contracts are very popular in foreign exchange market as well as interest rate bearing instruments. Most of the large and international banks quoted the forward rate through their ‘forward desk’ lying within their foreign exchange trading room. Forward foreign exchange

quotes by these banks are displayed with the spot rates.

Different types of forward: As per the Indian Forward Contract Act-1952, different kinds of forward

contracts can be done like hedge contracts, transferable specific delivery (TSD) contracts and non-transferable specific delivery (NTSD) contracts. Hedge contracts are freely transferable and do not

specify, any particular lot, consignment or variety for delivery. Transferable specific delivery contracts are though freely transferable from one party to another, but are concerned with a specific and predetermined consignment. Delivery is mandatory. Non-transferable specific delivery contracts, as the name indicates, are not transferable at all, and as such, they are highly specific.

Some other features of forward contract are as given below:

1.Agreement between the two counter parties.

2.Specifies a quantity and type of asset to be sold or purchased.

3.Specifies the future date at which the delivery and payment to be made.

4.Specifies the price at which the payment is to be made.

5.Obligates the seller to deliver the asset and also the buyer to buy the asset.

6.No money changes hands until the delivery date reaches, except for a s mall service fee, if there is.

Basic terms used in forward contract

Spot contract or cash contract:Contracts where delivery is made immediate within a short settlement period.

Spot market:Market where immediate buying and selling take place i.e. time ‘t’ between selling and buying process is equal to zero and the price is known as spot price.

Delivery price:Quoted price in the forward process.

Some important terminology frequently used in forwards contract

Long position: The party who agrees to buy in the future is said to hold long position.

Short position: The party who agrees to sell in the future is said to hold a short position.

The underlying asset: Any asset in the form of commodity, security or currency that will be bought and sold when the contract expires.

Future spot price: The spot price of the underlying asset when the contract expires.

The forward price: It is the agreed upon price at which both the counter parties will transact when the

contract expires.

Example of forward contract

An example would help illustrate the mechanics of a forward contract. Suppose on January 1, 2012 an Indian textile exporter receives an order to supply his product to a big retail chain in the US. Spot price of INR/US exchange rate isRs. 45/dollar.

After six months, the exporter will receive $1 million (Rs 4.5 crore) for his products. Since all his expenditure is in rupee term therefore he is exposed to currency risk. Let’s assume that his cost of production isRs. 4 crore. To avoid uncertainty, the exporter enters into a six-month forward contract with a bank (with some fees) atRs. 45 to a dollar. So the exporter is hedged completely.

If exchange rate appreciates toRs. 35 after six months, then the exporter will receiveRs. 3.5 crore after converting his $1 million and the restRs. 1 crore will be provided by the bank. If exchange rate depreciates toRs. 60/dollar then the exporter will receiveRs. 6 crore after conversion, but has to payRs.

1.5 crore to the bank. So no matter what the situation is, the exporter will end up withRs. 4.5 crore.

Advantages of forward contract

Protection against Exchange Rate Fluctuations: Forward contracts can be beneficial in the agricultural industry, and farmers use them to protect against the risk of crop prices declining before harvesting can be done. For example, a farmer plants a crop of wheat and expects the crop to yield 10,000 bushels at harvest time. To protect himself against the risk of the wheat price dropping, he will sell the entire

10,000 bushels that he expects to harvest to a buyer. The two parties make an agreement and fix the price

of a bushel of wheat, delivery to be made five months from the date of the transaction agreement. Money

does not change hands at this time. The farmer has protected himself from possible exchange rate

fluctuations and declines in the wheat market. Of course, he takes the risk that the price of wheat will

not go up.

Hedging against Risk

Risk management is the primary motivation for forward contracts. Companies use forward contracts to hedge their risk against foreign exchange. For example, a company based in the U.S. incurs costs in dollars for labor and manufacturing. It sells to European clients who pay in euros. The company has a lead time of six months to supply the goods. In this case, the company is at risk from uncertain market fluctuation of exchange rates. The company uses a forward contract to sell the product six months later at today's exchange rate. Apart from these advantages some other advantages of forward contract are:

- They can be matched against the time period of exposure as well as for the cash size of the exposure.

- Forwards are tailor made and can be written for any amount and term.

- Forwards are over-the-counter products.

- Forward contracts provide price protection

Gain on Long Position in Forward Contract

Gain on long position = Number of units (Future spot price – Future price or delivery price)i.e. Number of

units [ST – FtT (or K)]

Where, number of unit is per contract.

Gain on Short Position in Forward Contract

Gain on short position = Number of units (Future price –Future spot price or delivery price) i.e. Number

of units [ FtT(or K) – ST]

Where, number of unit is per contract.

Pay-off from Forward Contract

The gain attained or the loss incurred by the holder of a forward contract at delivery date. In general, the payoff from a long position in a forward contract (long forward contract) on one unit of its underlying asset or commodity is:

Payoff short position = ST - K

Where, ST is the spot price of the underlying at maturity of the contract K is the delivery price agreed

in the contract.

The holder of the long position is obligated to buy the underlying, trading at sport price ST, for the

delivery price K.

Conversely, the payoff from a short position in a forward contract (short forward contract) on one unit

of its underlying is:

Payoff long position = K - ST

The holder of the short position is obligated to sell the underlying, trading at sport price ST, for the

delivery price K.

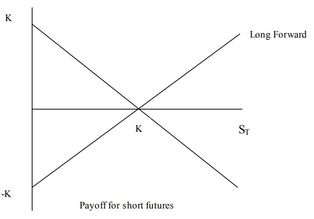

Payoff diagram of long forward and short forward

Figure shows a payoff diagram on a contract forward. Note that both the long and short forward payoff positions break even when the spot price is equal to the forward price. Also note that a long forward’s maximum loss is the forward price whereas the maximum gain is unlimited.

Figure-1 Payoff diagram of long forward and short forward Where ST is the spot price and k is the delivery price.

Getting out of Forward Contract

Parties to a futures contract may also terminate the contract prior to expiration through an offset. Offset is the transaction of a reversing trade on the exchange.

In other words, if you buy a futures contract and subsequently sell a comparable contract, you have offset your position and the contract is extinguished.

Offset trades must match in respect to the underlying asset, delivery dates, quantity, etc., or the original position will not be effectively terminated. In such cases, price movements in the original contract will continue to result in gains or losses. To extinguish default risk on a forward contract, a trader must place the reversing position with the same counterparty and under the same terms as in the originally contract. Obviously, this makes it difficult to get out of a forward contract prior to termination.

Forward contracts are negotiated agreements between buyer and seller. To enter into a forward contract, it is necessary to find someone who wants to buy exactly what you want to sell when and where you want to sell it. Without a formal exchange and clearing house to guarantee delivery and payment, there is always a chance that either the buyer or the seller will default on an obligation. If one of these counterparties fails, the other is still responsible for performing under the contract. Traders in forward contracts who re-enter the market to execute a reversing trade prior to the expiration date will effectively increase their default risk exposure because they will be dealing with two different counterparties, both of which have to live up to their ends of the bargain.

Futures Contract

A futures contract is an agreement between a buyer and a seller where the seller agrees to deliver a specified quantity and grade of a particular asset at a predetermined time in futures at an agreed upon price through a designated market under stringent financial safeguards. A futures contract, in other words,is an agreement to buy or sell a particular asset between the two parties in a specified future period at an agreed price through specified exchange. For example, the S&P CNX NIFTY futures are traded on National

stock exchange. This provides them transparency, liquidity, anonymity of trades and also eliminates the

counter party risks due to the guarantee provided by National Securities Clearing Corporation limited.

The standardized items in any Futures contract are

- Quantity of the underlying asset

- Quality of the underlying asset

- The date & month of delivery

- The units of price quotation & minimum change in price (tick size)

From the above, it is evident that financial futures termed as a notional commitment to buy or sell a standard quality of a financial instrument at a specified price on a specified future date. It means that

this market is rarely used for the exchange of financial instruments. In fact, financial futures markets are independent of the underlying assets.

In general, financial futures are not different from commodity futures except of the underlying asset; for example, in commodity futures, a particular commodity like food grains, metals, vegetables, etc. are traded whereas in financial futures, instruments

like equity shares, debentures, bond, etc. traded.

Types of Financial Future Contracts

Depending on the type of underlying asset, there are different types of futures contract available for trading. They are –

Interest rate futures

Interest rate futures are traded on the NSC. These are futures based on interest rates. In India, interest rates futures were introduced on August 31, 2009.The logic of underlying asset is the same as we saw in commodity or stock futures. In this case, the underlying asset would be a debt obligation, debts that move in value according to changes in interest rates (generally government bonds). Companies, banks, foreign institutional investors, non-resident Indian and retail investors can trade in interest rate futures. Buying an interest rate futures contract will allow the buyer to lock in a future investment rate.

Foreign currency futures

They trade in the foreign currencies, thus also known as Exchange rate futures. The MCX-SX exchange trades the following currency futures:

- Euro-Indian Rupee (EURINR),

- Us dollar-Indian rupee (USDINR),

- Pound Sterling-Indian Rupee (GBPINR) and

- Japanese Yen-Indian Rupee (JPYINR).

Stock index futures

Understanding stock index futures is quite simple if you have understood individual stock futures. Here the underlying asset is the stock index. For example – the S&P CNX Nifty popularly called the ‘nifty futures’. Stock index futures are more useful when speculating on the general direction of the market rather than the direction of a particular stock. It can also be used to hedge and protect a portfolio of shares. So here, the price movement of an index is tracked and speculated. One more point to note here is that, although stock index is traded as an asset, it cannot be delivered to a buyer. Hence, it is always cash settled. Both individual stock futures and index futures are traded in the NSE.

Bond index futures

These are based on particular bond indices, that is, indices of bond prices. As we know that prices of debt instruments are inversely related to interest rates, so the bond index is also related inversely to them. Example is the Municipal bond index futures based on US Municipal bond that is traded on the Chicago board of trade (CBOT).

Cost of living index futures

This is also known as Inflation futures. These futures contracts are based on a specified cost of living index, for example, consumer price index, wholesale price index, etc. these futures can be used to hedge against the unanticipated inflation which cannot be avoided. Hence such future contracts can be very useful to certain investors like provident funds, pension funds, mutual funds, etc.

Specifications of the futures market exchanges

All the futures contracts are initiated through a particular exchange. When a new futures contract is developed, an exchange must specify the underlying asset, size of the contract, how price will be quoted, where and when delivery will be made, and how price will be determined.

Stock exchanges perform the following functions:-

a) They provide and maintain a physical market place known as the floor where futures transactions are sold and purchased by the members of the exchange.

b) They maintain and enforce ethical and financial norms applicable to the futures trading undertaken on the exchange.

c) They make efforts to promote business interests of the members because the exchange’s main objective is to extend the facilities for such trading to its members.

Each exchange has usually membership organization whose members can be individuals or business organizations. Membership is limited to a specified number of seats. The members of the exchange have the right to trade on the floor of exchange, in turn, they agree to follow and abide by the rules of the exchange.

The Clearing House

An agency or separate corporation of a futures exchange responsible for settling trading accounts, clearing trades, collecting and maintaining margin monies, regulating delivery and reporting trading data. A clearing house is a financial institution that provides clearing and settlement services for financial and commodities derivatives and securities transactions. These transactions may be executed on a futures exchange or securities exchange, as well as offexchange

in the over-the-counter (OTC) market. Clearing houses act as third parties to all futures so that clearing house stands between two clearing firms (also known as member firms or clearing participants) and its purpose is to reduce the risk of one (or more) clearing firm failing to honor its trade settlement obligations. A clearing house reduces the settlement risks by netting offsetting transactions between multiple counterparties, by requiring collateral deposits (also called "margin deposits"), by providing independent valuation of trades and collateral, by monitoring the credit worthiness of the clearing firms, and in many cases, by providing a guarantee fund that can be used to cover losses that exceed a defaulting clearing firm's collateral on deposit. Also, it acts as a clearing firm.

Some of the important functions performed by the clearing house

- As clearing house give guarantee for all the transactions and acts as counterparty for all the transactions it will never have open positions in the market.

- It ensures that all parties adhere to the system and procedures so that various parties in the market can do trading smoothly which in turn leads to more confidence of the players on the markets and hence it increases liquidity in the market.

- It ensures a proper risk management system in place by stipulating that margin is maintained which is of two types initial and maintenance margin and hence accounting is done for all the gains and losses on daily basis and hence chances of default are reduced considerably.

- It ensures that delivery of the underlying asset is consistent in terms of quality, quantity, size etc. so that there is no confusion among parties, in other words all contracts are standardized.

Hedging using futures contract

Noting the shortcomings of the forward market, particularly the need and the difficulty in finding a counter party, the futures market came into existence. The futures market basically solves some of the shortcomings of the forward market. Futures contracts are one of the most common derivatives used to hedge risk. A futures contract is an arrangement between two

parties to buy or sell an asset at a particular time in the future for a particular price. The main reason that companies or corporations use future contracts is to offset their risk exposures and limit themselves from any fluctuations in price. The ultimate goal of an investor using futures contracts to hedge is to perfectly offset their risk. In real life, however, this is often impossible and, therefore, individuals attempt to neutralize risk as much as possible instead. For example, if a commodity to be hedged is not available as a futures contract, an investor will buy a futures contract in something that closely follows the movements of that commodity. To enter into a futures contract a trader needs to pay a deposit (called an

initial margin) first. Then his position will be tracked on a daily basis so much so that whenever his account makes a loss for the day, the trader would receive a margin call (also known as variation margin), i.e. requiring him to pay up the losses.

There are basically two types of hedges using futures contract

Short hedge: Short hedge is taking a short hedge position in the futures market. It is appropriate when someone expects to sell an asset he already owns and wants to guarantee the price. In general being short means having a net sold position, or a commitment to deliver. Thus here the main objective is to protect the value of the cash position against a decline in cash

price.

For example, Company X must fulfill a contract in six months that requires it to sell 20,000 ounces of silver. Assume the spot price for silver is $12/ounce and the futures price is $11/ounce. Company X would short futures contracts on silver and close out the futures position in six months. In this case, the company has reduced its risk by ensuring that it will receive $11 for each ounce of silver it sells.

Long hedge: long hedge is taking a long position in the futures market. It is a situation where an investor has to take a long position in futures contracts in order to hedge against future price volatility. A long hedge is beneficial for a company that knows it has to purchase an asset in the future and wants to lock in the purchase price. A long hedge can also be used to hedge against a short position that has already been taken by the investor. It is appropriate for someone who expects to buy an asset and wants to guarantee the price.

For example, assume it is January and an aluminum manufacturer needs 25,000 pounds of copper to manufacture aluminum and fulfill a contract in May. The current spot price is $1.50 per pound, but the May futures price is $1.40 per pound. In January the aluminum manufacturer would take a long position in May futures contract on copper. This lock in the price the manufacturer will pay.

If in May the spot price of copper is $1.45 per pound the manufacturer has benefited from taking the long position, because the hedger is actually paying $0.05/pound of copper compared to the current market price. However if the price of copper was anywhere below $1.40 per pound the manufacturer would be in a worse position than where they would have been if they did not enter into the futures contract.

Example of hedging strategy using futures

A farmer who has been on the fence about hedging decides to hedge his corn crop. He thinks that prices will remain around the current level or decrease in late August when he anticipates selling his new crop. The cash price for new crop corn is $5.52 and the September futures price is $6.28. The farmer anticipates that he will have 10,000 bushels of corn to sell. Since the farmer wants to protect himself against a decrease in prices, he will be a short hedger. His goal is to lock in the price of $5.52/bu for corn. Each corn futures contract contains 5,000 bushels. The farmer sells two September 2011 corn futures contracts at $6.28 on 2/23/11. It is now September and the farmer’s instincts held true. Cash corn prices are

currently at $5.00 and September futures are trading at $5.25. The farmer sells his grain in the cash market and offsets his position in the futures market on 8/28/11.

Table: Change in Basis

| Date | Cash | Future | Basis |

|---|---|---|---|

| 02/28/2011 | 5.52 | 6.28 | -.76 |

| 08/28/2011 | 5.00 | 5.25 | -.25 |

| = -.52 | = +1.03 | = .51 |

The farmer lost -.52 on the cash side, but his short futures position had a gain of 1.03. The net result of the hedge is a gain of 51 cents per bushel.

Example of currency rate hedging using currency futures:

Suppose that the 2 year interest rates in Australia and the United States are 5% and 7%, respectively, and the spot exchange rate between the Australian Dollar and the US dollar is 0.6200 USD per AUD.

Now the relationship between the forward exchange rate, F0 and the spot exchange rate, S0 is

F0 = S0(r-r1) T

So the two year forward exchange should be

0.62e (0.07-0.05)*2 = 0.6453

Again suppose that the 2 year exchange rate is less than 0.6453, say 0.6300, in this situation an arbitrageur can

1.Borrow 1,000 AUD at 5% per annum for 2 years, convert to 620 USD and invest the USD at 7%.

2.Enter into a forward contract to buy 1,105.17AUD for 1,105.17*0.63 =696.26 USD.

The 620 USD that are invested 7% grow to 620 e0.072 = 713.17 USD in 2 years. Of this696.26 USD are used to purchase 1,105.17 AUD under the terms of the contract. This is exactly enough to repay principal and interest on the 1.000 AUD that are borrowed (1,000 e0.052 = 1.105.17 the strategy thus give rise to a riskless profit of 713.17 – 696.26 = 16.91 USD

Again, suppose that the 2 year forward rate is greater than 0.6453, say 0.6600, in this situation an arbitrageur can

1.Borrow 1,000 USD at 7% per annum for 2 years, convert to 1,612.90 AUD and invest the AUD at 5%.

2.Enter into a forward contract to sell 1,782.53

AUD for 1,782.53*0.66 = 1,176.47 USD.

The 1,612.90 AUD that are invested at 5% grow to 1,612.90 e0.052 = 1,782.53 AUD in 2 years. The forward contract has the effect of converting this to 1,176.47 USD. The amount needed to pay off the USD borrowings is 1,000 e0.0721,150.27 USD. The

strategy therefore gives rise to a riskless profit of 1,176.47 – 1,150.27 = 26.20 USD

Payoff of Futures Contract

The payoff of futures contract on maturity depends on the spot price of the underlying asset at the time of maturity and the price at which the contract was initially traded. There are two positions that could be taken in futures contract

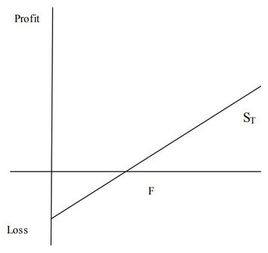

Long position: One who buys the asset at the future price take the long position. In general, the payoff for a long position in a futures contract on one unit isST-F

Where, F is the traded future price and ST is the spot price of the asset at expiry of the contract. This is because the holder of the contract is obligated to buy the asset. The following figure depicts the payoff diagram of investor who is long on a future contract.

Figure shows that investor makes a profit in long position if spot price at the expiry exceeds the future contract price and losses if opposite happens.

Short position:One who sells the asset at the future price takes the short position. In general the payoff for the short position in a futures contract is FST

Where, F is the traded future price and ST is the spot price of the asset at expiry of the contract. The figure below depicts the payoff diagram of investor who is short on a future contract

Figure-2 Payoff for long futures

Figure shows that investor makes a profit in long position if spot price at the expiry is below the future contract price and losses if opposite happens

Working of commodity futures market

Every day, people engage in activities that require the use of products. The raw materials that go into making these products are called commodities. Commodities are bought and sold in what is called the cash market. This is sometimes called the "spot market" because people pay in full for the commodity "on the spot." The principle of supply and demand governs the trading prices of commodities. If supplies are plentiful, prices will be low. If supplies are scarce, prices will be high.

Future traders

There are two types of traders in the futures markets, hedgers and speculators. Hedgers are primarily comprised of businesses that actually use the commodities they are trading. The hedgers' objective is to lock in a favorable contract price that protects them against unforeseen fluctuations in the spot market. Hedgers are willing to give up the possibility

of lower spot prices to avoid the detrimental effects of exorbitantly high spot prices. Farmers, mining companies, and oil drillers are examples of hedgers who use futures contracts as a kind of cost insurance policy for their businesses.

In contrast to the hedger, the speculator never uses commodities in any manufacturing capacity. Speculators trade strictly for the prospect of acquiring profits. By watching the markets closely every day, a speculator can take advantage of small fluctuations in a futures contract's price by buying and selling at lower or higher points during the life of the contract.

Advantages of Futures Contract

Futures are highly leveraged investments: To own a futures contract, an investor only has to put up a small fraction of the value of the contract (usually around 10%) as margin. In other words, the investor can trade a much larger amount of the commodity than if she bought it outright, so if she has predicted the market movement correctly, her profits will be

multiplied (ten-fold on a 10% deposit). This is an excellent return compared to buying a physical commodity such as copper or wheat.

Speculating with futures contracts is basically a paper investment: The actual commodity being traded in the contract is only exchanged on the rare occasion that delivery of the contract takes place. Since the average individual investor is a speculator, a futures trade is purely a paper transaction and the term "contract" is only used as the futures contract has an

expiration date.

Liquidity: Since there are huge amounts of futures contracts traded every day, futures markets are very liquid. This ensures that market orders can be placed very quickly as there are always buyers and sellers of a commodity. For this reason, it is unusual for prices to suddenly jump or fall dramatically, especially on the nearer contracts (those which will expire in the next few weeks or months).

Commission charges are small: compared to other investments and are paid after the position has ended. Commissions vary widely depending on the level of service given by the broker.

Disadvantages of Futures Contract

High risk of loss: Before becoming too excited about the substantial returns possible from commodity trading, it is a good idea to take a long, sober look at the risks. Reward and risk are always related. It is unrealistic to expect to be able to earn above-average investment returns without taking above-average risks as well. Commodity trading has the reputation of

being a highly risky endeavor. It is true that a high percentage of traders eventually lose money. Many people have lost substantial sums. Leverage is a double edge sword, it can either make you rich or make you lose your shirt and more.

Margin Call:In the futures market, rather than providing a down payment like on a house, the initial margin required to buy or sell a futures contract is solely a deposit of good faith money that can be drawn on by your brokerage firm to cover losses that you may incur in the course of futures trading. They are typically about five percent of the current value of the

futures contract. If and when the funds remaining available in your margin account are reduced by losses to below a certain level known as the maintenance margin requirement your broker will require that you deposit additional funds to bring the account back to the level of the initial margin. Or, you may also be asked for additional margin if the exchange or your

brokerage firm raises its margin requirements. Requests for additional margin are known as margin calls.

Difference between Forwards & Futures Contract

The main differentiating feature between futures and forward contracts are as given below:

Definition: A forward contract is an agreement between two parties to buy or sell an asset (which can be of any kind) at a pre-agreed future point in time at a specified price. On the other hand, a futures contract is a standardized contract, traded on a futures exchange, to buy or sell a certain underlying instrument at a certain date in the future, at a specified price.

Structure & Purpose: Forward contracts are customized to customer needs. Usually no initial payment required. These are usually used for hedging while in case of futures they standardized, initial margin payment required and are usually used for

speculation.

Transaction method: Forwards are negotiated directly by the buyer and seller but futures are quoted and traded on the Exchange.

Guarantees: In case of forwards no guarantee of settlement until the date of maturity only the forward price, based on the spot price of the underlying asset is paid. On the other hand both parties must deposit an initial guarantee (margin) in case of futures. The value of the operation is marked to market rates with daily settlement of profits and losses.

Contract Maturity: Forward contracts generally mature by delivering the commodity. Its expiry datedepends on the transaction. But future contracts may not necessarily mature by delivery of commodity. Its expiry date is standardized.

Closing a Position:To close a position on a futures trade, a buyer or seller makes a second transaction that takes the opposite position of their original transaction. In other words, a seller switches to buying to close his position, and a buyer switches to selling. For a forward contract, there are two ways to close a position — either sell the contract to a third party, or get into a new forward contract with the opposite trade.

Liquidity:It is easy to buy and sell futures on the exchange. It is harder to find counterparty over-thecounter to trade in forward contracts that are nonstandard. The volume of transactions on an exchange is higher than OTC derivatives, so futures contracts tend to be more liquid.

Picking the right Hedging tool

Futures contracts are special types of contracts that obligate the seller to deliver the commodity on a specific date in the future. For this reason, many people confuse futures contracts with forward contracts. While the basic concepts are similar, there are actually many differences between futures contracts and forward contracts.

One of the primary differences between a futures contract and a forward contract is the fact that forwards can only transact when they are purchased and on the settlement date. When it comes to futures, however, the can actually rebalance every day. Since forwards cannot rebalance, it is possible for a large differential to develop between the delivery price and the settlement price. This is particularly true if the price of the underlying asset changes drastically. As a result, investment in a forward contract is far riskier than forwards.

Since futures are rebalanced on a daily basis, the credit risk of this type of investment is virtually eliminated. This is because the person holding the futures contract must update the price to be equivalent to how much a forward would be purchased for on the same day. As a result, the amount of additional money that is due on the settlement day is usually very small. Furthermore, the futures-settlement failure risk is actually carried by the exchange rather than by the individual.

Another difference between forwards and futures is the fact that futures can only be traded on an exchange. Forwards, on the other hand, are always traded over-the-counter or by simply having the two parties sign a contract. Since futures must be traded on an exchange, the exchange acts as the counter party for the trade. Yet, the exchange does not have a net position, which means the buyer and seller actually do not know who they traded to. Since forwards are completed over-the-counter or through a contract signed by both parties, the buyer and seller work directly with each other in order to complete the exchange.

The fact that futures are very standardized also sets them apart from forwards. Although some forwards can be standardized, some are also unique. Furthermore, if the contract has to be physically delivered, forward contracts specify precisely who the delivery must be made to. The entity receiving the futures contract, on the other hand, is selected by the clearinghouse. The clearinghouse is a company that specializes in financial services and provides clearing and settlement services for futures transactions and other financial transactions.

Although the basic concept behind futures and forwards is quite similar, there are many subtle differences that must be considered when making an investment in these types of contracts. Most importantly, we need to weigh the risks associated

with each type of contract in order to determine which the best type of investment for us is. If you are willing to take a risk, forwards might be right for you. If you are interested in an investment with very little risk and that is easy to complete, however, futures contracts might be a better choice.

Summary & Conclusions

Derivatives have totally changed the working scenario of financial markets. Derivatives are those hedging tools that help an organization or an individual to effectively transfer risk. Particularly futures and forward contracts have earned an extremely significant place among all the financial products. They are easy to trade and provide an opportunity to transfer risk, from those who want to avoid it and to those who want to accept it. Although there are certain disadvantages of futures but at the same time the advantages they have, make them essential to be traded in the market. Using futures and forward contracts, an individual can hedge various types of risks like commodity risk, interest rate risk, and currency risks etc. The role of derivatives as hedging tool assumes that derivatives trading do not increase market volatility and risk; moreover they minimize the risk and serve as route for hedging the various types of risk.

References

1.Journal of Comprehensive Research by PetrosJecheche University of Zimbabwe: Basics of futures and forward contracts discussed from a risk management perspective

2.Gupta S.L.(2005), Financial Derivatives: Theories, Concepts and Problems

3.Hull John C. (sixth edition, 2005) Options, Futures and other Dervatives

4.AshutoshVashishtha, Faculty College of Management, Shri Mata Vaishno Devi University (SMVDU)Katra. (J&K) India ‘Development of Financial Derivatives

Market in India’- A Case Study

5.Dr. Kamleshgakhar and Ms. Meetu, derivatives market in india: evolution, trading mechanism and future prospects available at www.indianresearchjournals.com

6.http://www.schuermaninsurance.com/futures/forwardcontracts-vs-futures.asp

7.http://www.answers.com/Q/What_are_the_advantages_and_disadvantages_of_forward_contract

8.http://www.ehow.com/info_8454326_advantagesdisadvantages-forward-contracts.html

9.http://www.danielstrading.com/strategies/2011/02/28/hedging-with-commodity-futures-its-all-about-managingprice-risk/

10.http://www.investopedia.com/terms/l/longhedge.asp

11.http://www.uic.edu/cuppa/pa/academics/Duplicate/Lectures, Outlines and Handouts/Public Finance/Asset Pricing-

%20Dennis%20Pelletier%20of%20North%20Carolina%20State%20University/Hedging%20using%20Futures.pdf

12.http://futures.tradingcharts.com/tafm/tafm7.html

13.http://www.letslearnfinance.com/various-functions-ofclearing-house.html

Jayanta Chakraborti

Associate Professor, Chandigarh University.

Jayanta Chakraborti is Associate Professor of Business Analytics and Digital Marketing at Chandigarh University. He holds a Bachelor’s degree in Mechanical Engineering from TEC Agartala, MBA from IMI Europe, MA in Economics from Devi Ahilyabai University Indore, Diploma in French from Delhi University and Certification in German from Max Mueller Munich.